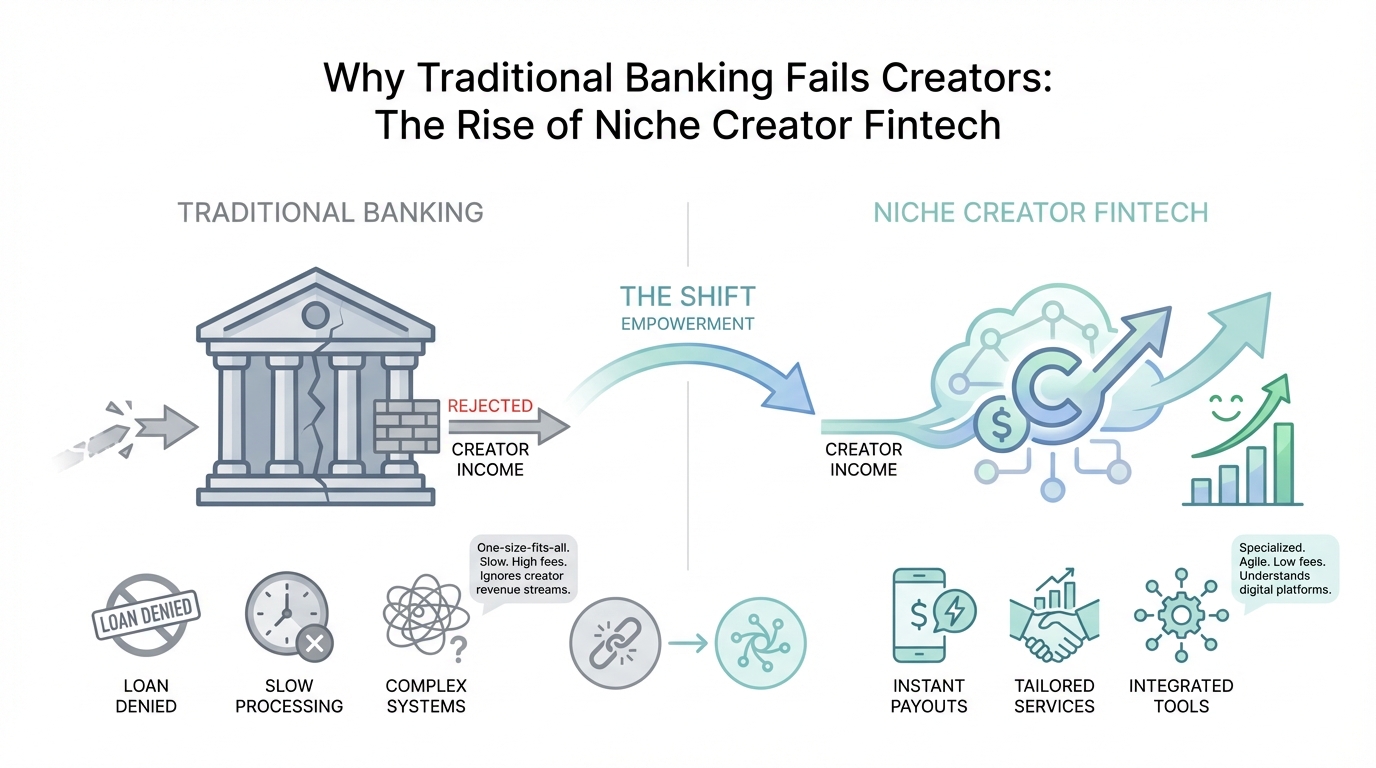

Imagine you have sold several companies, invested in multiple successful startups, and have enough liquid capital to buy a luxury condo in Miami outright in cash. You approach one of the largest banks in the world for a mortgage, only to hear: "I’m sorry, but we can’t give you a loan. You don't have W-2 income." This isn't a hypothetical scenario; it is the reality for modern founders and the portfolio-job generation. The traditional financial system was built for a world that no longer exists—a world where you stayed at one company for 40 years, retired with a gold watch, and lived on a stable salary. Today, as the creator economy explodes, the gap between traditional banking and the needs of 1099 earners has become a chasm, paving the way for a new era of creator economy fintech.

The Underwriting Problem: Why Wealth Isn’t Enough

The core of the issue is the underwriting for entrepreneurs. Large institutions like Chase or Bank of America rely on rigid, legacy rails that prioritize steady, predictable W-2 income above all else. This results in absurd situations where a YouTuber making $1 million a year might be stuck with a meager $5,000 credit limit. The traditional system doesn't know how to value a YouTube channel's recurring revenue or a founder's equity. It looks at the past—your credit score and your pay stubs—rather than your current cash flow or future earning potential.

We see this systemic failure repeatedly. Take the example of Josh Fabian, the founder of Metafy. Despite building an incredible company backed by the world's leading VCs, he struggled to rent an apartment in New York because of his past credit history. Even offering to pay a full year of rent upfront in cash wasn't enough to overcome the legacy underwriting hurdles. This illustrates that the rails of the entire financial ecosystem are fundamentally broken for where the world is headed. The modern earner is more likely to have 1099 income from various sources—consulting, sponsorships, or digital products—than a single paycheck from a corporate giant.

Applying the Disruptive Innovation Framework to Modern Banking

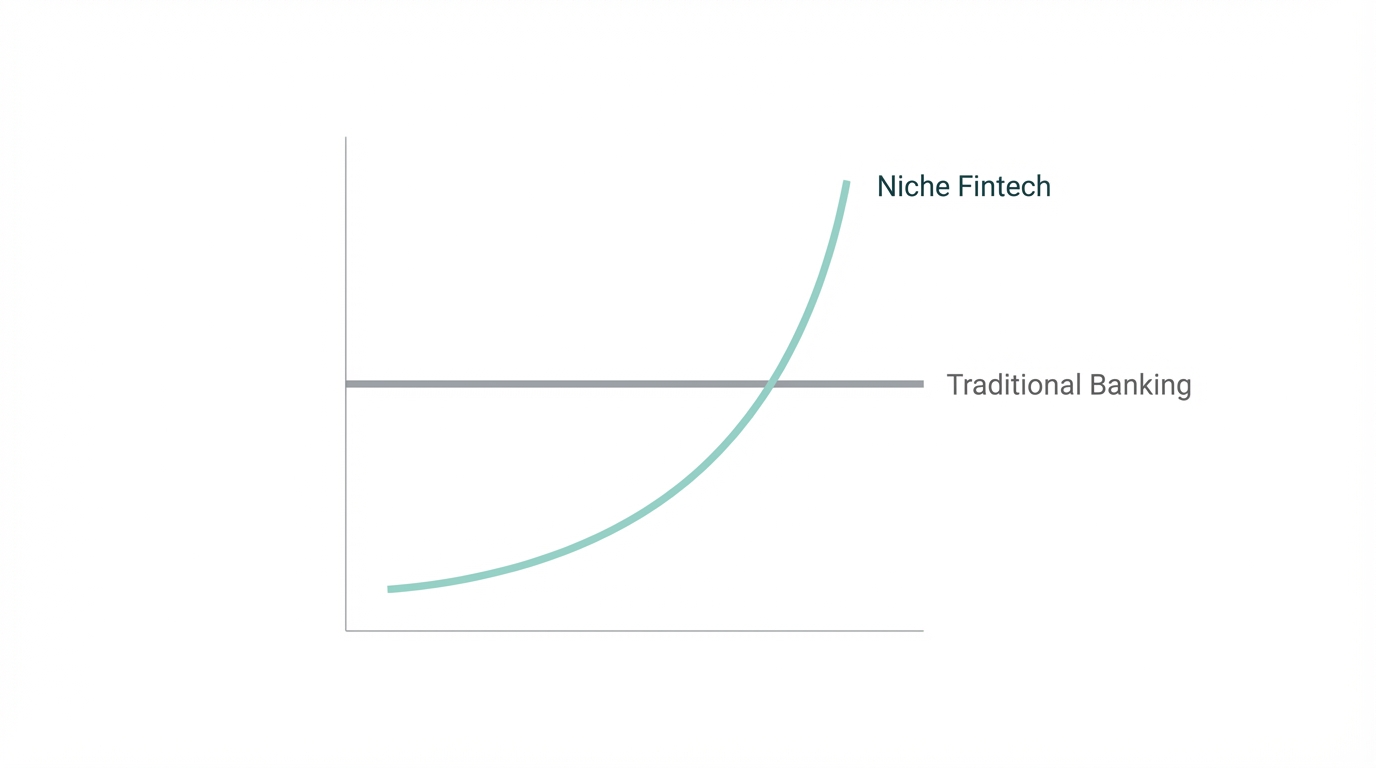

To understand why niche banks are winning, we have to look at disruptive innovation examples. Harvard Business School professor Clayton Christensen pioneered the theory that small upstarts can disrupt massive incumbents by targeting underserved or overserved market segments. Traditional banks are classic incumbents; they have massive ecosystems, but they are often too slow and too regulated to pivot. They overserve the "safe" corporate employee while almost entirely ignoring the high-growth, high-risk-profile entrepreneur.

Disruption starts with a wedge. A startup doesn't try to be everything to everyone on day one. Instead, it identifies a single customer archetype—like a startup founder or a TikTok influencer—and builds the absolute best minimum viable product for them. By focusing on a specific niche, they can create alternative underwriting models that the big banks wouldn't dare touch. Once they own that niche, they expand outward to take over the entire ecosystem. This is how the "unbundling" of the big bank begins. The same way Meta Ads Manager allowed small businesses to target hyper-specific audiences, niche fintechs are targeting hyper-specific financial profiles.

Case Study: How Karat and Mercury Used a Niche Wedge

Two prime examples of this disruption are Karat and Mercury. Karat recognized that the fintech for influencers space was virtually non-existent. They saw million-dollar creators being treated like high-risk gamblers by traditional banks. Karat’s wedge was simple: build a credit card designed specifically for creators. Instead of looking at FICO scores, they look at social media metrics, engagement rates, and platform-specific income. They understand that for a creator, spending money on production isn't a luxury—it's a deductible business expense that fuels further growth.

Then there is Mercury, which transformed banking for creators and startups by removing the friction of opening an account. While a legacy bank might require a physical visit and weeks of paperwork, Mercury allows founders to apply from anywhere in the world in ten minutes. Their focus on beautiful, intuitive design and a product that "just works" has made them the default choice for the new generation of entrepreneurs. They don't just offer an account; they offer a toolset that helps startups manage their cash flow and scale without the administrative headache. This is the disruptive innovation playbook in action: find the pain point, remove the friction, and serve the niche better than anyone else.

The Unbundling of Investing: Beyond Stocks and Bonds

The decline of the "gold watch" era isn't just about how we earn; it is about how we invest. For decades, the financial industry pushed the 60/40 portfolio (60% stocks, 40% bonds). But as Howard Lindzon pointed out, this was essentially a bundled product that didn't give investors real choice. The modern era is defined by the unbundling of the S&P 500. Investors no longer want to passively own a basket of companies that might include brands they find ethically or financially questionable. They want to curate their own "gardens."

This shift has led to the rise of investable assets across the board. From fractionalizing high-end cars via platforms like Rally to investing in NFTs and crypto, everything is now a potential trade. In the past, only the ultra-wealthy had access to these types of alternative assets. Now, platforms are democratizing access, allowing a 20-year-old to buy a fraction of a classic Porsche or stake their crypto for a yield. We are moving from a world of passive accumulation to a world where speculation is entertainment and everyone is a "man in the arena." While legacy media calls this dangerous, the new generation sees it as a necessary education in risk management.

Founder Playbook: Identifying Underserved Archetypes

Step 1: Deep Immersion

You cannot identify a niche from the outside. You have to immerse yourself in the community. This might mean joining Discord servers, monitoring Reddit threads, or physically moving to where your target audience lives. When the team behind the app Islands wanted to build for college students, they didn't just stay in San Francisco—they moved to Tuscaloosa, Alabama, to live and breathe the college experience. By being present, they discovered nuances in how students communicated that they never could have found in a Silicon Valley office.

Step 2: Listen for the "Arbitrage" Point

Look for areas where there is a massive gap between perceived risk and actual risk. For example, legacy banks perceive 1099 creators as high-risk because their income is variable. However, an AI-powered creator discovery platform like Stormy AI can analyze engagement data, follower growth, and historical content quality to show that a creator is actually a stable, growing business. If you can use data to underwrite risk better than a bank, you have an arbitrage opportunity. This applies to managing creator relationships too; tools like Stormy AI can help brands search, vet, and manage outreach to these creators, effectively acting as a CRM for the new economy.

Step 3: Build the Software Around the Community

Don't build software and then look for a community. Build the community—or find an existing one—and then build the software that solves their specific problems. Whether it's the biker community, the NFT "Twitterati," or gig economy drivers, each niche has a specific "language" and a specific set of hurdles. Your product needs to speak that language and provide the "warm and fuzzy" feeling that a generic bank never can.

The Future of Credit for the Portfolio-Job Generation

The W-2 era is effectively over for a significant portion of the high-output workforce. We are entering the age of the business of one. In this world, your "job" is a portfolio of different activities. You might manage a newsletter through AppSumo deals, run a YouTube channel, and do freelance consulting. In this environment, underwriting for entrepreneurs must become more dynamic. It will be based on real-time data, social capital, and historical cash flow rather than a static credit score.

This shift is also why fintech for influencers is just the beginning. We will see "vertical banks" for every major trade and community. There will be banks for doctors, banks for plumbers, and banks for digital nomads—each with custom-tailored credit products and financial tools. The goal of these platforms is to lower the friction of starting. As we've seen with Mercury, when you make it easier for people to handle their finances, you free them up to build great products and grow their businesses.

Conclusion: The Niche Will Inherit the Earth

The failure of traditional banking isn't just an inconvenience; it's a massive market signal. The creator economy fintech revolution is proof that the old ways of underwriting and service are no longer sufficient. By applying disruptive innovation examples, startups are finding that the best way to win is to start small, serve a specific community perfectly, and use data to see what others miss. Whether you are a founder looking for the next "wedge" or a creator looking for a bank that finally understands you, the future is niche, unbundled, and digital. The gold watch has been replaced by the equity stake, and the traditional bank is being replaced by a code-driven, community-focused financial partner.