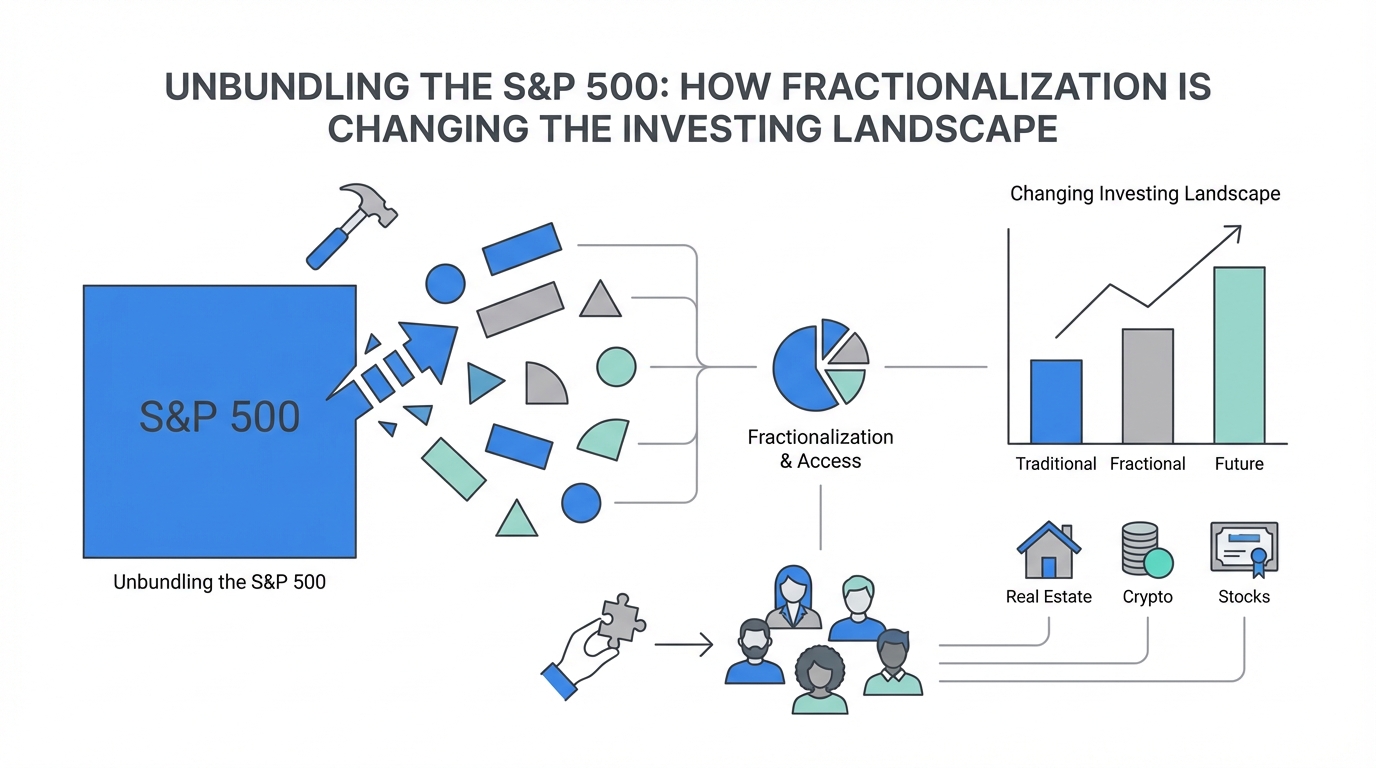

For decades, the standard advice for any individual looking to grow their wealth was simple: buy a low-cost index fund and wait forty years. This "set it and forget it" approach, championed by the giants of the 20th century, created a generation of passive investors. But the world has moved beyond the gold-watch-at-retirement era. Today, we are witnessing a fundamental shift in how people view ownership, risk, and portfolio management. The unbundling the S&P 500 is no longer just a theoretical concept discussed by venture capitalists—it is an active movement where fractional investing platforms are dismantling the monolithic index in favor of curated, fervent, and highly active communities.

The End of the Passive Investing Lie

One of the most provocative ideas surfacing in modern fintech is that passive investing is a lie. As Howard Lindzon noted in his analysis of the market, even the most traditional vehicles like the S&P 500 are, in reality, high-turnover quant funds. Every quarter, committees at major institutions decide which companies are kicked out and which are added based on performance and market capitalization. When you buy into a traditional index, you aren't just buying the market; you are buying an active portfolio packaged as passive to lower your psychological barrier to entry.

For the modern investor, this "black box" approach is becoming increasingly frustrating. Why should an investor who believes in ethical banking be forced to hold shares in legacy institutions they despise? The traditional financial rails, much like those used by Mercury to disrupt old-school banking, were designed for a world where technology was slow and fractionalization was impossible. In the past, you couldn't buy 0.001% of a share of Apple, so you bought the index. Today, technology has removed that barrier, exposing the inherent flaws in the passive vs active investing debate. If you can choose exactly what you own down to the penny, why would you let a faceless index decide for you?

This realization is driving a move toward active portfolio gardening. Rather than letting their wealth sit in a stagnant pool, investors are beginning to prune their holdings. They are removing underperformers or companies that don't align with their values, effectively creating their own personalized indices. This shift is empowered by the same low-friction philosophy that allows founders to start companies instantly without the red tape of traditional banking.

Unbundling Vanguard: The Rise of Personalized Gardening

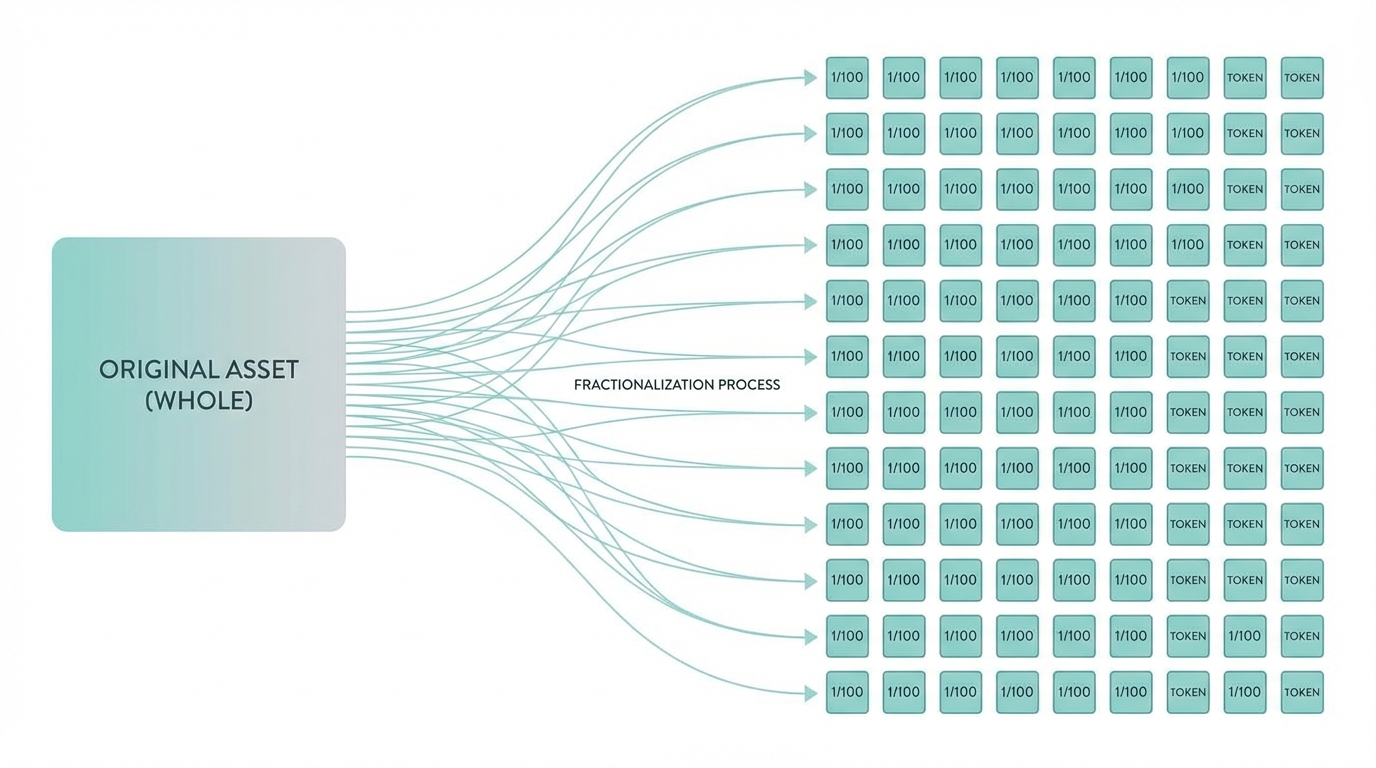

If Vanguard and the great index fund pioneers had opened their APIs a decade ago, companies like Robinhood might never have needed to exist. The unbundling of Vanguard is essentially a technology play. Large incumbents hoarded the ability to fractionalize assets, forcing retail investors to buy the whole bundle or nothing at all. But as the fintech business models evolved, startups realized that the real demand wasn't for the bundle—it was for the individual components.

Apps like Rally Road and Robinhood have effectively democratized the "gardening" of portfolios. Investors can now go into the market and buy fractional interests in everything from high-growth tech stocks to vintage Ferraris. This isn't just about diversification; it's about personal agency. The modern investor wants to know exactly what they own. They want to be able to tell the legacy banks to take a hike while keeping the winners that they actually believe in.

This movement mirrors the way entrepreneurs source tools today. Instead of buying a massive, bloated software suite, they use platforms like AppSumo to find specific, high-utility tools that solve exact problems. The unbundling the S&P 500 is the financial equivalent of moving from a legacy ERP to a stack of specialized, best-in-class SaaS applications. It is about precision over proximity. By utilizing fractional investing platforms, the barrier to entry for alternative asset classes has dropped to zero, allowing someone with $100 to have the same portfolio composition as a billionaire.

Speculation as Entertainment: The Rise of the Gladiator Investor

We have entered an era where speculation has become entertainment. In ancient Rome, the populace watched gladiators in the arena to pass the time; today, we watch the "gladiator investor" on platforms like Reddit and Stocktwits. When an investor loses $30,000 on a high-risk trade and posts the "loss porn" for thousands of people to see, they aren't just losing money—they are performing. They are the man in the arena, and the community celebrates their courage (or lack thereof) in real-time.

This cultural shift is a direct result of the gamification of finance. When you remove the friction of trading, the act of investing becomes a hobby. It becomes a social experience. The rise of the Stocktwits community showed that people don't want to talk about stocks in a vacuum; they want to talk about them with like-minded individuals who speak the same language. The dollar-sign ticker was more than just a search feature—it was a tribal marker.

For the younger generation, getting "punched in the face" by a bad trade is a rite of passage. It is education through participation. Losing $5,000 at age 22 is a far better financial education than sitting through a lecture on compound interest. These investors are learning the rules of the game by playing it, not by watching from the sidelines. As more alternative asset classes become available, the game only gets more complex and more engaging. To reach these users, companies often need specialized help; tools like Stormy AI can help source and manage UGC creators at scale who can speak to these specific, high-energy financial subcultures.

Investing in 'Fervent Communities'

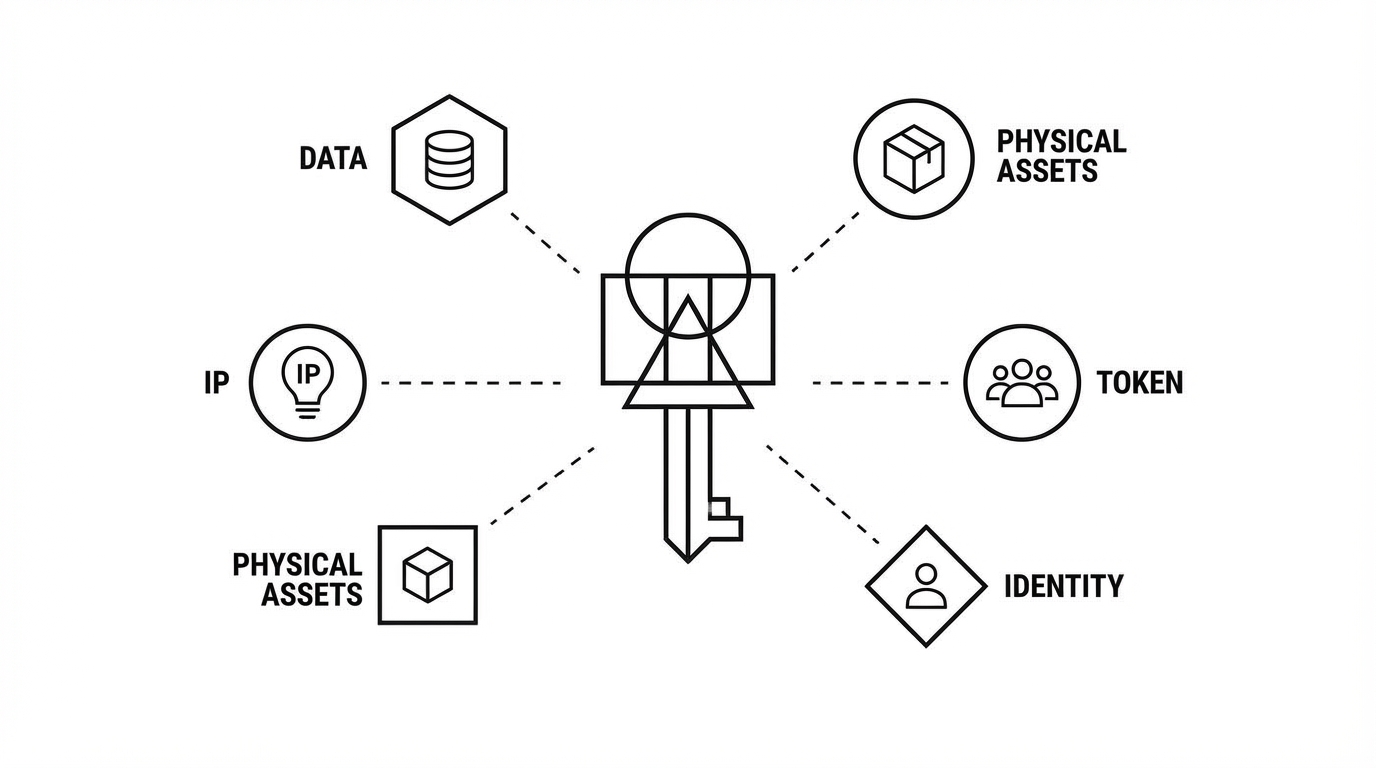

The next great investable asset class isn't a stock or a bond—it’s the fervent community. Whether it’s a biker gang in Connecticut, a specific NFT Discord, or a subreddit dedicated to vintage watches, these communities represent concentrated economic energy. When a group of people is deeply obsessed with a niche, they spend money, they create content, and they drive value. Unbundling the S&P 500 allows us to invest directly in these pockets of passion rather than a diluted average of the entire economy.

Consider the power of a community like the one built around Stocktwits. By focusing on the "dollar sign" language of traders, they created a home for a specific archetype. The same logic applies to Web 3.0 and NFTs. These aren't just digital images; they are membership tokens for communities that operate 24/7, 365 days a year. Investing in an NFT is often an investment in the social capital and the collective effort of that group.

For founders building in this space, the challenge is no longer just building the software; it's about immersing in the community. You cannot build a financial product for creators if you don't understand that a YouTuber making $1 million a year might still have a $5,000 credit limit at a traditional bank. The legacy system's inability to underwrite these new archetypes is the greatest opportunity for fintech today. By using an AI-powered creator discovery platform, brands can vet and identify the leaders of these fervent communities to build trust and drive adoption for new fractional investing platforms.

A Founder's Guide to Building a Fractionalized Marketplace

Building a platform for alternative asset classes requires a different playbook than traditional fintech. You aren't just building a ledger; you are building a cultural engine. Here is the step-by-step approach for founders looking to disrupt the passive vs active investing landscape.

Step 1: Identify an Underserved Archetype

Traditional banks like Chase or Bank of America overserve some and massively underserve others. Look for the "misfits" of the financial world—creators, immigrants, or 1099 contractors. As seen with the success of Mercury, providing a frictionless on-ramp for a specific group (like startups) creates a powerful wedge. Understand their specific pain points: Do they need faster payments? Do they need higher credit limits based on non-traditional data? Use this as your starting point.

Step 2: Start with the Community, Then Build Software

Don't build in a vacuum. Immersion is the only way to find product-market fit. Whether it's hanging out in college towns to understand student finances or joining every relevant Discord, you must teleport yourself into the room where the conversation is happening. Dissect the language they use and the problems they complain about. Only then should you write your first line of code. Leverage tools like AppSumo to automate the busy work so you can focus 100% on this community research.

Step 3: Design for Engagement and Speculation

The unbundling the S&P 500 works because it makes investing fun. Your UI should not look like a 1990s brokerage account. It should feel intuitive, social, and perhaps even a bit competitive. Incorporate social proof, real-time feedback, and the ability for users to share their "wins" and "losses" easily. If you are targeting the creator economy, ensure your product fits their lifestyle—mobile-first, beautiful aesthetics, and instantly shareable.

Step 4: Scale via Niche Influencers

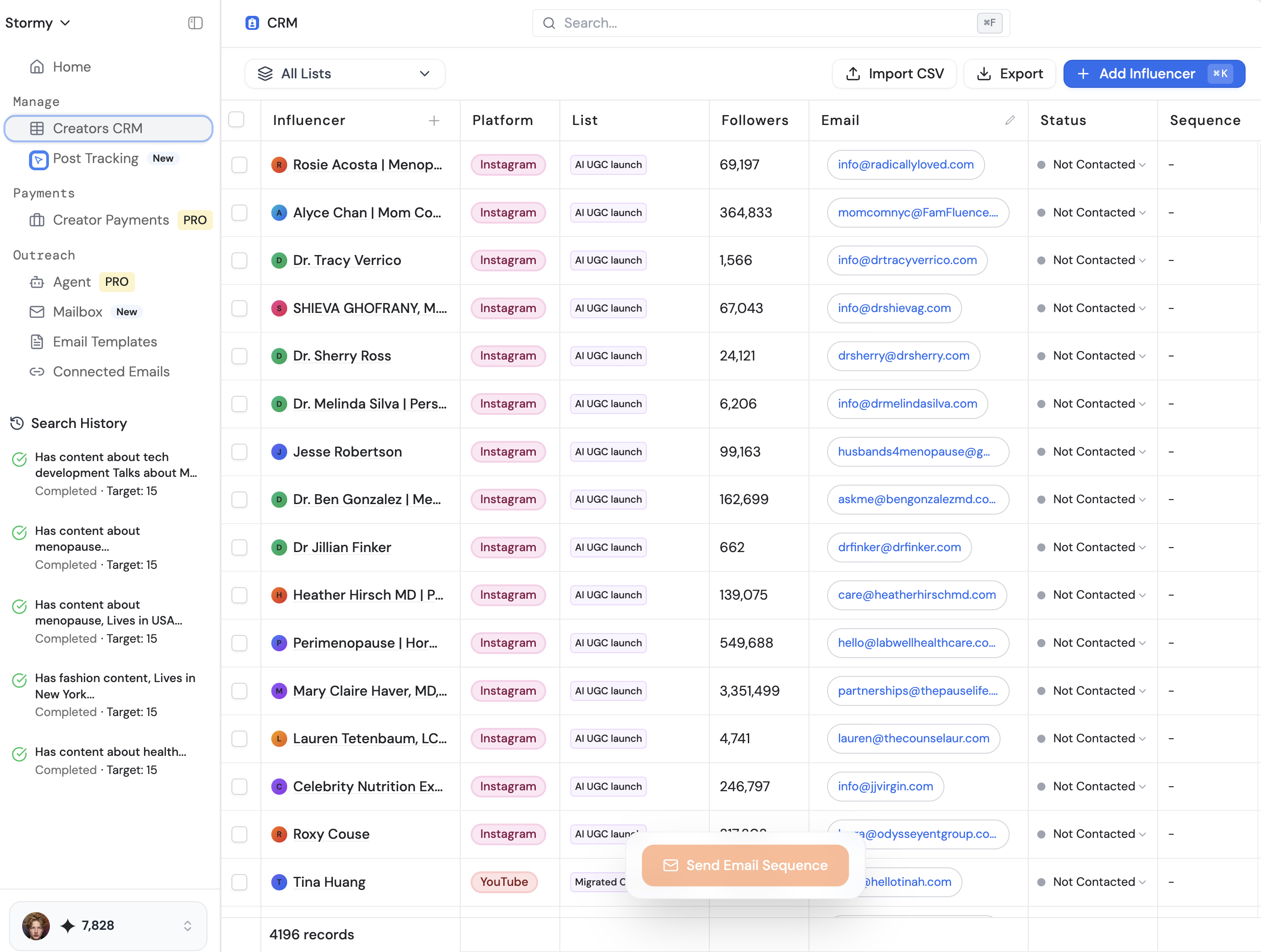

Once you have a product that resonates, you need to reach the wider community. Don't waste money on broad Facebook ads. Instead, find the micro-influencers who already lead the community you are targeting. A creator CRM like the one provided by Stormy AI can help you track these relationships, manage payments, and monitor campaign performance across TikTok, YouTube, and LinkedIn. This ensures that your outreach is personalized and effective.

Conclusion: The Future of Ownership is Fractional

The unbundling the S&P 500 is not just a trend; it is the inevitable conclusion of a world with zero-cost fractionalization. We are moving away from a world of "average" returns toward a world of high-conviction ownership. Whether it’s owning a piece of a 1960s Porsche on Rally Road or backing a favorite creator's new venture, the way we invest is becoming a reflection of our identities.

For the investor, the takeaway is clear: stop being passive. Start gardening your portfolio and exploring the alternative asset classes that the legacy system tried to keep for itself. For the founder, the opportunity is even larger: find a fervent community, solve their unique financial problems, and build the next pillar of the unbundled economy. The tools exist, the capital is available, and the "room where it happens" is now open to everyone. It's time to stop watching the gladiators and step into the arena yourself.