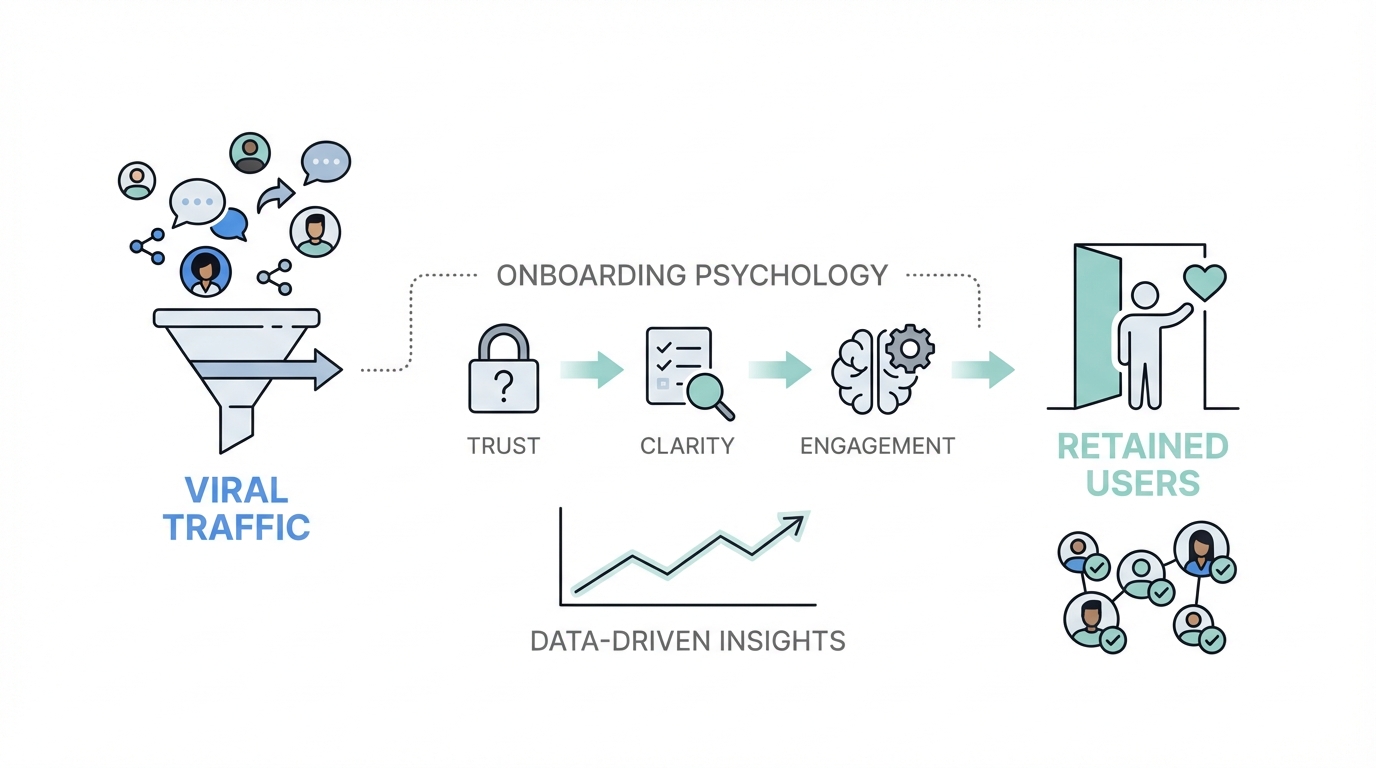

Imagine a user scrolling through TikTok, their brain primed for high-speed, low-stakes entertainment. They see a viral hook—perhaps a narrative about a billionaire nanny and the investing habits of the ultra-wealthy. Intrigued, they click the link in the bio, download your fintech app, and are immediately hit with a 20-field KYC (Know Your Customer) form requiring their Social Security Number and bank login. The excitement vanishes, and so does the user. This gap between the viral hook and the high-friction reality of financial services is where most fintech growth engines stall. Success in the modern app economy isn't just about getting the download; it is about user conversion optimization that maintains psychological momentum through the most difficult parts of the funnel.

Bridging the Viral Gap: The Reality of High-Friction Onboarding

Fintech apps face a unique challenge that simple productivity or entertainment apps do not: trust and complexity. While a user might impulsively download a photo editor, they are far more mindful when it comes to their money. According to recent growth research, mobile app retention strategies for finance must account for the fact that users are naturally skeptical. They are looking for a reason to leave the moment they see a screen asking for personal data. To bridge this gap, your onboarding must mirror the content that brought them there in the first place.

If your top-of-funnel traffic is coming from platforms like TikTok or Instagram, your onboarding needs to feel like an extension of those platforms. The goal is to move the user from a state of passive consumption to active participation without triggering their internal alarm bells. This requires a deep understanding of fintech gamification and the psychology of small wins. Platforms like Stormy AI enable fintech brands to source creators who maintain this visual consistency from ad to app.

The Psychology of Story-Style Onboarding

One of the most effective app onboarding best practices currently being used by industry leaders is the transition from single-screen, text-heavy signups to multi-screen, story-style interactions. For years, the conventional wisdom was to reduce the number of taps. However, UI/UX research suggests that increasing the number of screens can actually improve conversion if those screens reduce cognitive load.

Why More Screens Can Mean Better Conversion

When you pack four or five value propositions onto a single screen, the user stops reading. They see a wall of text and instinctively look for the 'Skip' button. By contrast, a 10-screen onboarding flow that uses large graphics, minimal text, and story-driven progression keeps the user moving. They are used to the story format from apps like Snapchat or Instagram. By clicking the right side of the screen to flip to the next insight, they are intuitively walking through your value prop rather than being forced to study it.

Visual Storytelling and Micro-Animations

Using vibrant colors, animations, and even meme-ified stock references (like Netflix or Tesla) can keep a Gen Z or Millennial audience engaged. These visual cues signal that the app is modern and relatable, contrasting with the 'stale' feel of legacy banking apps. Every tap is a micro-commitment that brings them closer to the actual account creation, making the final step—entering personal info—feel like a natural conclusion rather than a sudden barrier.

Psychological Triggers: Urgency and Social Proof

To keep a user moving through a long onboarding flow, you must inject psychological triggers at strategic intervals. Two of the most powerful are urgency through compounding and social proof through reviews.

The Power of Compounding Visuals

Nothing creates urgency like the fear of missing out on money. A common tactic is showing a comparison graph: 'If you invest $X at age 18, you'll have $1,000,000 by 65. If you wait until age 30, you'll only have $340,000.' This visual representation of the cost of waiting shifts the user's mindset from 'I'll do this later' to 'I need to start today.' This is a cornerstone of user conversion optimization because it provides a logical reason to endure the high-friction KYC steps immediately.

Social Proof at the Point of Friction

Just before you ask for the most sensitive information, such as a Social Security Number, you should present social proof. Including a screen with customer reviews or trusted partner logos (like Yahoo Finance or Y Combinator) gives the user the confidence they need to proceed. When they see that thousands of others have successfully and safely used the app, the perceived risk of sharing their data drops significantly.

Incentive Alignment: The Case for 'Free Stock' Over 'Free Cash'

Incentives are a standard part of mobile app retention strategies, but the type of incentive matters immensely. In the fintech world, there is a constant debate: do you give away free cash or free stocks? While cash is universally understood, receiving a fractional share of stock is often the superior choice for long-term retention.

When a user receives $5 in cash, they may just see it as a discount or a one-time bonus. When they receive a fractional share of Apple or Amazon, they become a 'shareholder.' They start checking the stock price. They feel a sense of ownership. This aligns the incentive with the long-term behavior you want to encourage: regular investing. By gamifying the acquisition of these stocks—perhaps through 'loot boxes' or rewards for completing educational modules—you create a feedback loop that keeps them coming back to the app daily.

Friction as a Feature: The 'No-Button' Strategy

It sounds counter-intuitive, but sometimes adding friction can actually increase the quality of your retained users. A fascinating experiment in app onboarding best practices involves removing the 'Get Started' or 'Continue' button from the initial onboarding screens. When there is no button to click, the user is forced to absorb the information on the screen to understand how to move forward.

By relying on the swipe or tap-to-advance mechanics of stories, you ensure the user isn't just mindlessly clicking through to the end. They are 'consuming' the value prop. This leads to a more informed user who understands why they are signing up, which significantly reduces churn in the first 30 days. This level of fintech gamification respects the user's intelligence while guiding their behavior.

The Playbook for Scaling Creator-Led Growth

Building a world-class onboarding funnel is useless if you don't have a consistent stream of high-intent traffic. The most successful fintech apps today are using an organic-to-paid feedback loop. This involves hiring a fleet of micro-influencers to produce high volumes of content—often up to 60 videos per month—to test which narratives resonate.

The Micro-Influencer Retainer Model

Instead of hiring one mega-influencer for $50,000, smart brands hire 20 micro-influencers on a retainer plus CPM bonus model. You might pay a $1,000 retainer for 60 videos, then offer bonuses ($2-$4 CPM) for videos that hit over 100,000 views. This incentivizes the creator to focus on virality and quality, rather than just fulfilling a contract. To manage this at scale, tools like Stormy AI allow brands to discover and vet micro-influencers across TikTok and YouTube, ensuring they find creators who actually reach their target demographic.

Transitioning Organic to Paid

Once an organic video goes viral, you don't just let it die. You take that asset and run it as a focused ad via Meta Ads Manager or Google Ads. Because the content has already been pre-validated by the organic algorithm, your CAC (Customer Acquisition Cost) is likely to be much lower. Using Apple Search Ads in tandem with these viral narratives ensures that when users search for your app after seeing a video, you own the top spot.

Conclusion: The 90-Day Consistency Rule

Converting viral traffic into retained users is not a one-time hack; it is a process of continuous refinement. Whether you are tweaking your paywall pricing or testing a new narrative about 'billionaire habits,' the key is consistency. Most growth engines fail because the founders stop testing after 30 days. It often takes a full 90-day cycle of daily content and onboarding iterations to find the 'golden' path that turns a casual scroller into a lifelong investor. By combining story-style onboarding, strategic psychological triggers, and a robust creator management system, you can build a fintech app that doesn't just grow—it lasts.