For decades, the financial technology sector has been obsessed with the next generation. Startups have poured billions into banking for teens, credit builders for Gen Z, and gamified trading apps for millennials. However, this hyper-fixation on youth has created a massive blind spot: the 65+ demographic. Often referred to as a "demographic burden" by economists due to shifting population ratios, this generation is actually the wealthiest in history, controlling nearly two-thirds of the wealth in the United States. As we look toward 2050, the population of adults over 65 is expected to double, reaching nearly 90 million people. The opportunity for fintech for older adults is no longer just a niche—it is the next frontier of global wealth management.

The $45 Billion Security Deposit Opportunity

One of the most archaic corners of the American financial system is the real estate security deposit. Currently, there is an estimated $45 billion tied up in security deposits across the U.S., most of which sits in dormant, low-interest checking accounts. For the aging population, many of whom are downsizing or transitioning into luxury rentals, this represents a significant pool of idle capital that is being eroded by 8.7% inflation. The traditional model involves a tenant writing a physical check to a landlord, who then holds it in a separate account for years, returning it only when the lease ends—often with a lower purchasing power than when it was first deposited.

There is a massive opening for a modern security deposit platform that treats these funds as assets rather than stagnant liabilities. Imagine a system where the tenant can choose to put their deposit into alternative assets, equities, or even crypto. In this "win-win" scenario, the landlord and tenant could split the upside of the appreciation. If the deposit grows by 20%, the landlord takes a small cut for the risk, the tenant keeps the rest, and the platform manages the smart contracts to ensure the original deposit amount is always protected. This type of financial products for retirees moves away from the "stodgy" banking of the past and toward a more flexible, internet-native approach to real estate liquidity.

Crypto for Seniors: Why the "Grandpa Myth" is Wrong

There is a persistent and patronizing myth that crypto for seniors is a non-starter because older adults "don't get technology." In reality, the 65+ demographic is increasingly curious about digital assets but lacks the specific tooling and trust-based interfaces required to participate safely. High-net-worth seniors are often looking for ways to diversify their portfolios, and many are actively seeking information on crypto tax implications and long-term holding strategies. The problem isn't a lack of interest; it's a lack of senior financial literacy tech that doesn't make them feel ridiculed or vulnerable to fraud.

The next generation of digital wallets needs to move from being simple storage tools to becoming "smart wallets" with predictive technology. For an older investor, a taxable event like swapping Bitcoin for a physical asset or a $10,000 investment can have significant consequences. A senior-friendly wallet should act as a "tax man on the shoulder," alerting the user in real-time to the likely tax implications of a transaction before it is executed. By integrating tools like CoinTracker directly into the UI, fintech companies can build the trust necessary to activate the massive wealth held by the aging population.

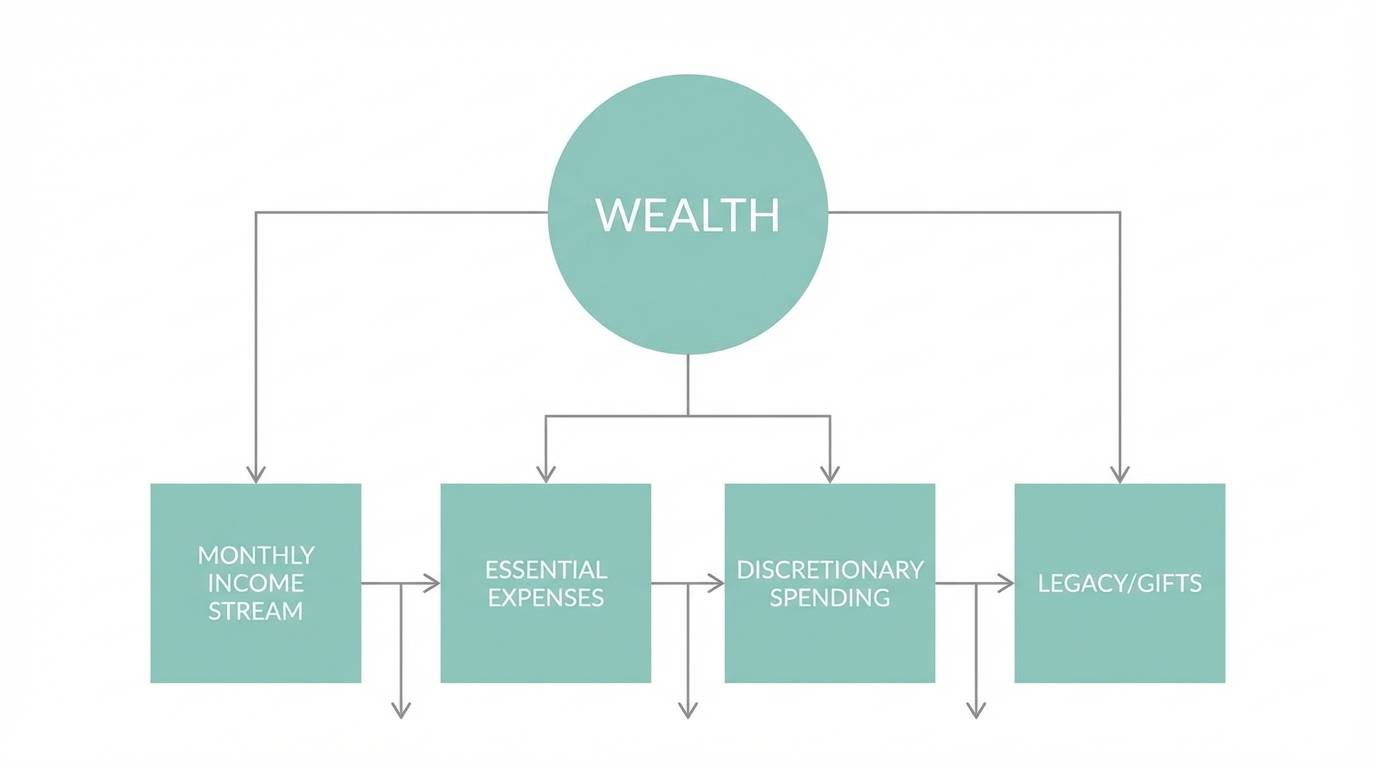

The Decumulation Challenge: From Saving to Spending

Most wealth management for aging population models are focused on accumulation—how to save enough to hit a "monthly nut." However, there is a psychological gap that the industry has largely ignored: decumulation. Many seniors who have lived frugally for 40 years to build a nest egg find it mentally taxing to shift into a "lavish spending" mindset. They have the capital, but they lack the permission and the tools to spend it down effectively to enhance their quality of life. This is where fintech for older adults can step in, creating "lavish retirement" trackers or "Me-Budgets" that encourage seniors to splurge on experiences and family rather than hoarding cash for an inheritance their children may not even want.

This shift requires a community-first approach. Just as Chief created a high-end network for professional women, there is a clear opening for a Chief-like platform for seniors. This wouldn't be a stodgy "senior center" for bingo; it would be an elite, application-only community for high-performing older adults to discuss wealth management, philanthropy, and lifestyle design. To reach this audience effectively, brands are increasingly looking toward UGC (User-Generated Content) and influencer marketing tailored to older demographics. AI-native platforms like Stormy AI can help source and manage specialized UGC creators who speak directly to the 65+ market, ensuring that marketing feels authentic rather than patronizing.

Unbundling AARP and the "Senior Living" Monolith

For decades, AARP has been the primary aggregator for older adults, generating over $1.7 billion in annual revenue. However, much like the unbundling of Craigslist led to the rise of Airbnb and Uber, the unbundling of the "senior" category is inevitable. AARP is a monolithic brand that many older adults find cringeworthy because it signals that "life is over." Modern entrepreneurs are finding success by taking specific components of the senior experience—dating, mentorship, niche travel, or financial products for retirees—and building standalone, high-quality brands around them.

Consider the "unbundling" of the nursing home. Traditional senior living facilities vertically integrate housing, nutrition, and social calendars, often resulting in a "lowest common denominator" experience like bingo nights. A more innovative approach is the experience-as-a-service model, where companies provide elite social programming and cultural events to seniors who want to remain in their own homes or in decentralized housing. Companies like Sylva are already experimenting with rolling up micro-communities, showing that there is massive liquidity and demand for niche, high-trust environments for the aging population.

Security, Trust, and High-End Usability

Finally, any successful fintech for older adults must solve the paradox of security versus usability. While older adults are more susceptible to certain types of fraud, they also have the lowest patience for complex, multi-factor authentication systems that feel like obstacles. The goal is to build a predictive trust layer. This involves using AI to monitor for anomalous patterns—such as a sudden attempt to move a large portion of a retirement fund—while maintaining a clean, accessible interface. Using specialized marketing talent from platforms like MarketerHire can help startups position these security features as a luxury service rather than a technical burden.

Moreover, the "demographic dividend" of the next twenty years suggests that the most successful companies will be those that facilitate intergenerational wealth transfer and mentorship. There is a desire for older adults to share their wisdom and assets with younger generations in real-time, rather than waiting for a probate court to handle a will. Platforms that allow for tenant-landlord asset sharing or peer-to-peer mentorship connections (similar to a LinkedIn for retirees) will tap into a deep psychological need for purpose and legacy. As Alive Ventures has noted, every great startup idea for this space comes from talking to hundreds of older adults to understand where they feel most "ignored" by modern design.

Conclusion: The Future of Senior Wealth

The 65+ demographic is not a monolithic group of tech-averse retirees; they are a powerhouse of capital and life experience waiting for products that treat them with respect and sophistication. From crypto for seniors that integrates real-time tax planning to real estate platforms that unlock billions in stagnant deposits, the opportunities are vast. By focusing on wealth management for aging population and moving away from the patronizing "senior center" tropes, fintech founders can build high-loyalty, high-LTV businesses that serve a truly underserved market. The winners in this space will be those who recognize that the "Silver Tsunami" is actually a golden opportunity for innovation.