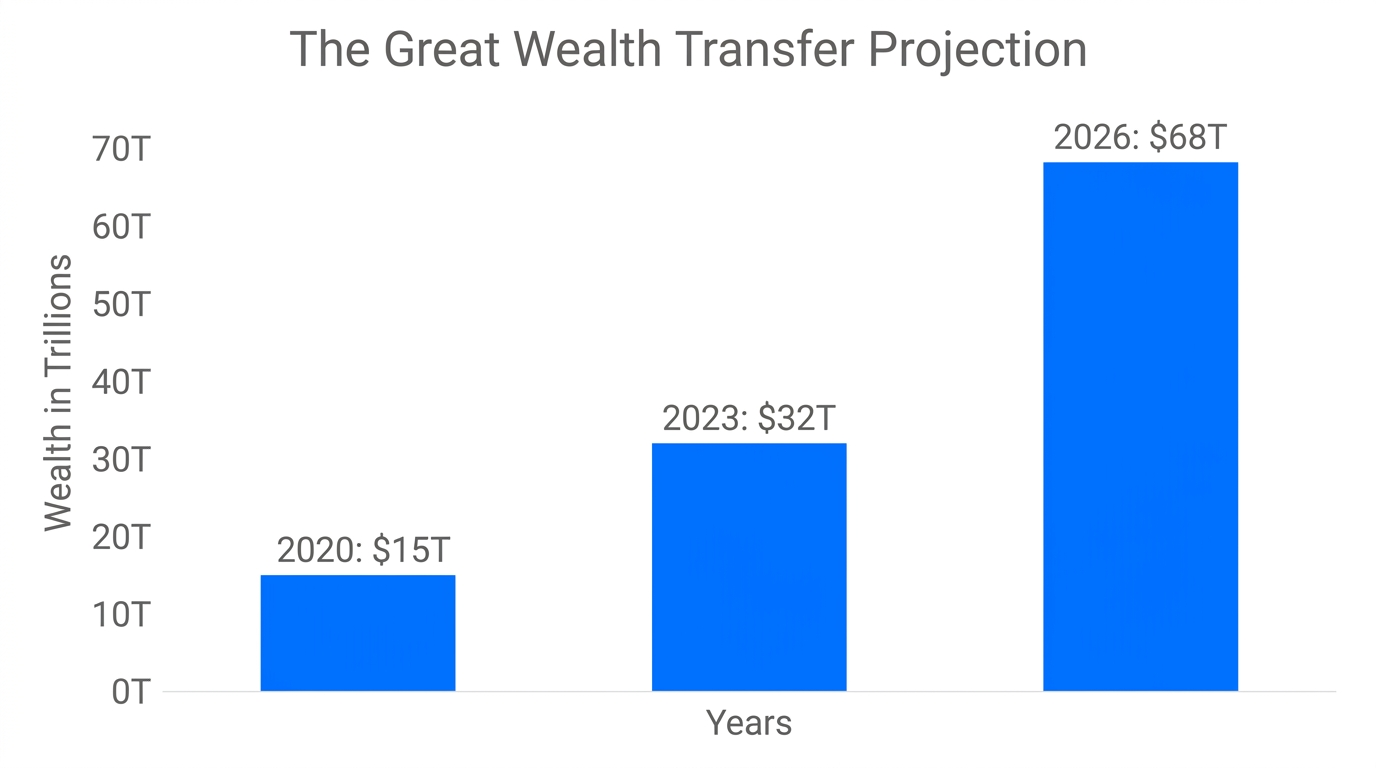

In 2026, the financial landscape is no longer being reshaped—it has been entirely rebuilt. We are currently witnessing the peak of the Great Wealth Transfer, where an estimated $20 trillion to $50 trillion is shifting from Boomers to Millennials and Gen Z. This isn't just a change in who holds the capital; it’s a radical shift in how that capital is managed, traded, and grown. For fintech giants like Robin Hood and Coinbase, the goal isn't just to be a better bank; it's to become the default operating system for the next generation's economic life. Success in this era is dictated by a mix of psychological rewards, high-velocity distribution, and the creation of 'cult' brand loyalty that traditional institutions simply cannot replicate.

The 2026 Wealth Transfer: Positioned as the New Default

Understand the massive tailwinds driving the upcoming shift in generational wealth.

The 2026 wealth transfer represents the largest liquidity event in human history. As trillions move into the hands of digital natives, the 'boring' financial models of the past are being discarded in favor of platforms that offer utility, speed, and social status. For a brand to win this segment, it must understand that Gen Z does not view a brokerage account as a utility—they view it as an extension of their digital identity. This is why Robin Hood has successfully transitioned from a simple trading app to a comprehensive financial suite offering 401ks, credit cards, and even home mortgages.

As younger investors inherit this capital, they gravitate toward platforms they already trust. Most Gen Z users started with small check deposits or crypto trades on Shopify storefronts or through digital wallets. By the time they receive a significant inheritance, the switching cost is already too high. They aren't moving their money to Charles Schwab or Morgan Stanley; they are staying where their direct deposit, credit card, and crypto portfolio already live. This is the ultimate distribution strategy: capture the user when they have $100, and you will own them when they have $1,000,000.

"The 2026 Wealth Transfer isn't just a change in account balances; it's a total migration of trust from the 'man in the suit' to the 'app in the pocket.'"Gamified Referrals: The 'Scratch-Off' Psychology of Viral Growth

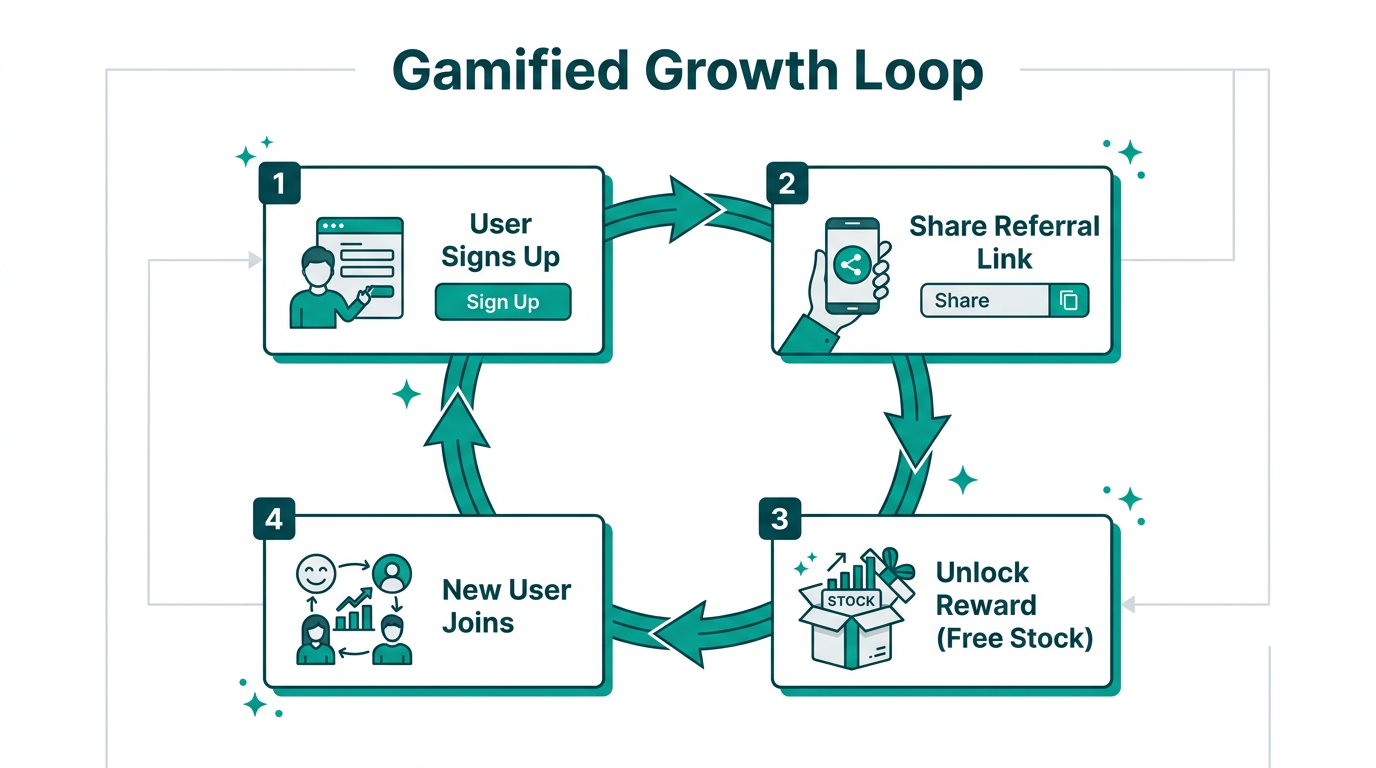

One of the most effective components of the Robin Hood growth strategy has been its mastery of psychological triggers. Early in its lifecycle, Robin Hood pioneered the 'scratch-off' referral mechanic. Instead of a standard $10 credit, users were given a digital card to 'scratch,' revealing a random share of stock. This created a variable reward loop, similar to the mechanics found in gaming or gambling, which triggered high-velocity social sharing.

This strategy aligns with the Law of the Opposite, a core concept from Al Ries and Jack Trout's 22 Immutable Laws of Marketing. When you aren't the market leader, you don't try to be better—you try to be the antidote. While legacy banks focused on stability and 'seriousness,' Robin Hood embraced being the opposite: fun, accessible, and high-energy. This wasn't a mistake; it was a deliberate move to frame the old guard as 'slow and out-of-touch,' effectively capturing the retail investor segment that felt ignored by Wall Street.

The Super-App Moat: Coinbase’s Multi-Revenue Strategy

Analyzing what creates a defensible business moat in the modern financial landscape.While many fintechs struggle with single-product dependency, a Coinbase marketing analysis reveals a much more sophisticated 'Super-App' moat. By 2026, Coinbase has diversified into nine distinct revenue lines, including their core exchange, staking services, institutional custody, and international derivatives. This diversification creates a massive competitive advantage: they can afford to lose money on customer acquisition in one area because the Lifetime Value (LTV) across the ecosystem is so high.

This 'Super-App' approach is the modern equivalent of the 'Lovers' line of products created by food scientist Tom Ryan at Pizza Hut. Ryan realized that there wasn't one 'perfect' product; there were perfect clusters of products. Similarly, Coinbase doesn't just serve 'crypto investors.' They serve the institutional staker, the retail degen, and the corporate treasurer. By providing a 360-degree financial ecosystem, they make it nearly impossible for a user to leave. This is how you build generational defensibility in a crowded market.

Trust vs. Utility: Winning the Retail Investor

Why users are gravitating toward specific platforms they trust for financial management.In app distribution 2026, the biggest challenge for fintech is the tension between trust and utility. Users want the 'high-velocity' features—fractional shares, 24/7 crypto trading, and prediction markets—but they also need to know their life savings are secure. The winners are those who can package complex financial security inside a 'cute' and user-friendly interface. This often involves highlighting FDIC insurance limits and 2FA protocols in a way that doesn't overwhelm the user.

However, the aesthetic of the app can actually be a double-edged sword. For older HNWIs (High Net Worth Individuals), a 'too-friendly' UI can feel like a toy, leading to skepticism. But for Gen Z, the 'ugly' legacy banking websites feel like a security risk. They associate bad design with bad technology. Platforms like Stormy AI are often used by these fintech brands to find creators who can bridge this gap—influencers who can explain the 'boring' security features in a way that feels native to social platforms like TikTok and YouTube.

"If your app looks like a toy but acts like a vault, you've solved the Gen Z distribution puzzle. If it looks like a vault but acts like a toy, you've lost."Network Effects and the Rise of 'Cult' Brands

In the current year, fintech brands are no longer just companies; they are movements. A major part of the Gen Z financial marketing playbook is the use of 'retail energy.' This is the phenomenon where a stock or platform becomes a part of a user's social identity. We see this with Tesla and OpenAI, where the founder-led transparency creates a sense of belonging among the user base. When Brian Armstrong or Elon Musk tweets, it moves the needle because the audience feels they are part of a shared mission.

This 'Cult' status creates a network effect that is nearly impossible to disrupt. When a brand like David Protein (founded by RX Bar creator Peter Rahal) can do $200 million in sales by its second year, it's not just because the product is good—it's because they leaned into the 'Law of the Opposite' and ran toward the criticism. Fintechs are doing the same: leaning into being 'the platform for the people' against the 'elites' of Wall Street, often fueled by retail investor momentum.

| Feature | Legacy Banks | Stormy AI Enabled Fintechs |

|---|---|---|

| Customer Acquisition | Direct Mail & TV Ads | AI-Powered Influencer Discovery |

| User Onboarding | Paperwork & Branches | Gamified Viral Loops |

| Product Range | Single Vertical (Savings) | Super-App Ecosystem |

| Brand Loyalty | Transactional | Cult / Community Energy |

The Playbook for Fintech Customer Acquisition in 2026

If you are building or marketing a fintech platform this year, your fintech customer acquisition strategy must follow this clear hierarchy of steps:

- Identify the Friction: Find the 'unsolved problem' in a category that others think is 'solved' (e.g., Tom Ryan putting cheese *inside* the crust).

- Embrace the Law of the Opposite: Don't try to be a 'better' version of the market leader. Be the obvious alternative.

- Build the Super-App Moat: Don't settle for one revenue stream. Launch complementary products to increase switching costs.

- Leverage Retail Energy: Use founder-led transparency and influencer partnerships on Stormy AI to build a brand that people want to talk about, not just use.

Conclusion: The Future of Generational Wealth

The 2026 wealth transfer is a once-in-a-lifetime opportunity to reset the financial hierarchy. Robin Hood and Coinbase have shown that by combining super-app mechanics, psychological rewards, and a 'cult-like' brand affinity, you can capture the next generation of wealth before they even know they have it. As the trillion-dollar shift continues, the platforms that win will be those that treat finance not as a series of transactions, but as a dynamic, high-velocity social experience. Whether you are an app developer or a marketer using tools like Instantly for outreach, the lesson is clear: if you want to own the future of money, you must first own the interface through which people experience it.