Disrupting Legacy Industries: The Ramp Guide to B2B Go-To-Market Strategy in 2026

Discover how Ramp's B2B go-to-market strategy disrupted legacy fintech. Explore the software-led tactics and customer retention strategies winning in 2026.

In 2019, two founders sat in a room and asked a question that would sound delusional to most: Can we build a billion-dollar company in just 18 months? Most founders aim for a decade of slow growth; Eric Glyman and Karim Atiyeh reverse-engineered a B2B go-to-market strategy built for pure velocity. By 2021, they hadn't just hit that billion-dollar valuation—they had shattered it, reaching an $8.1 billion valuation in under two years from incorporation. In 2026, Ramp stands as the ultimate case study in how modern software can topple centuries-old giants like Chase and Amex by identifying 'paper cut' pain points and offering a superior, utility-led distribution model.

Identifying the 'Boring' Opportunity: Why Unsexy Problems are Goldmines

Eric Glyman shares why pursuing unglamorous business models often yields the greatest rewards.

In the high-stakes world of fintech marketing 2026, many startups fail because they try to invent entirely new behaviors. Ramp did the opposite. They looked at the most 'boring' and 'unsexy' corner of business operations—expense management and accounting—and realized it was a goldmine of friction. While legacy banks were focused on rewards points and prestige, Ramp focused on the misery of manual receipt chasing and the 'paper cuts' that bleed finance teams dry every month.

Glyman realized that the founders of their competitors—Amex, Citi, and Chase—literally wore top hats. These companies were built in the 1800s. Their edge was brand longevity and massive distribution, but their weakness was technological stagnation. If you look at your parents' bank account from 30 years ago, it looks remarkably similar to a bank account today. This lack of innovation created a massive gap for a Ramp competitive analysis that prioritized software over status. By using tools like Notion to document these tiny frustrations, Ramp built a product that solved the day-to-day agony of the average CFO.

"The world is moving faster than ever. We wanted to either make this company huge quickly or fail really quickly. It turns out, solving 'boring' problems is the fastest path to huge."

Software as the Trojan Horse: Winning Market Share from Giants

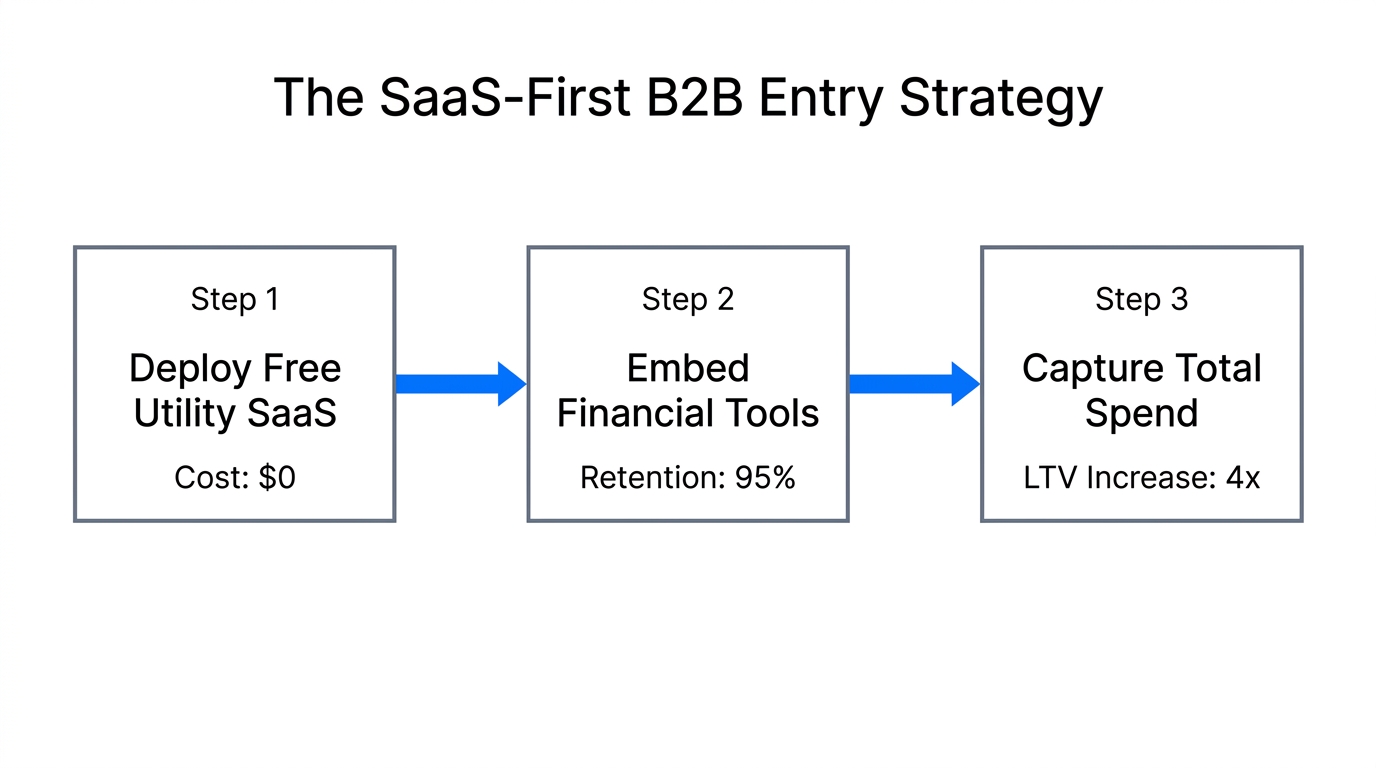

The core of Ramp's disruptive marketing tactics was the realization that the credit card itself was just a commodity. The real value was the software layer sitting on top of it. In a traditional model, a bank gives you a card and hopes you spend more. Ramp flipped this by building software that actually helped you spend less. This was their Trojan Horse: they gave away world-class expense management software for free, which naturally led businesses to adopt their card as the primary spending vehicle.

This is a classic B2B go-to-market strategy shift. Instead of leading with a sales pitch for a financial product, they led with a utility-based tool. This mirrors how modern platforms like Shopify won the e-commerce market—not by just processing payments, but by providing the entire operating system for a business. When your software handles the accounting, the audit logs, and the SaaS spend tracking, the financial service becomes the default choice. Businesses in 2026 are increasingly looking for tools that integrate into their workflow, much like how teams manage their projects in Linear or Monday.com.

The Interchange Model: The Engine of 'Free' Software

Learn the complex reality of how credit card companies actually make their money.

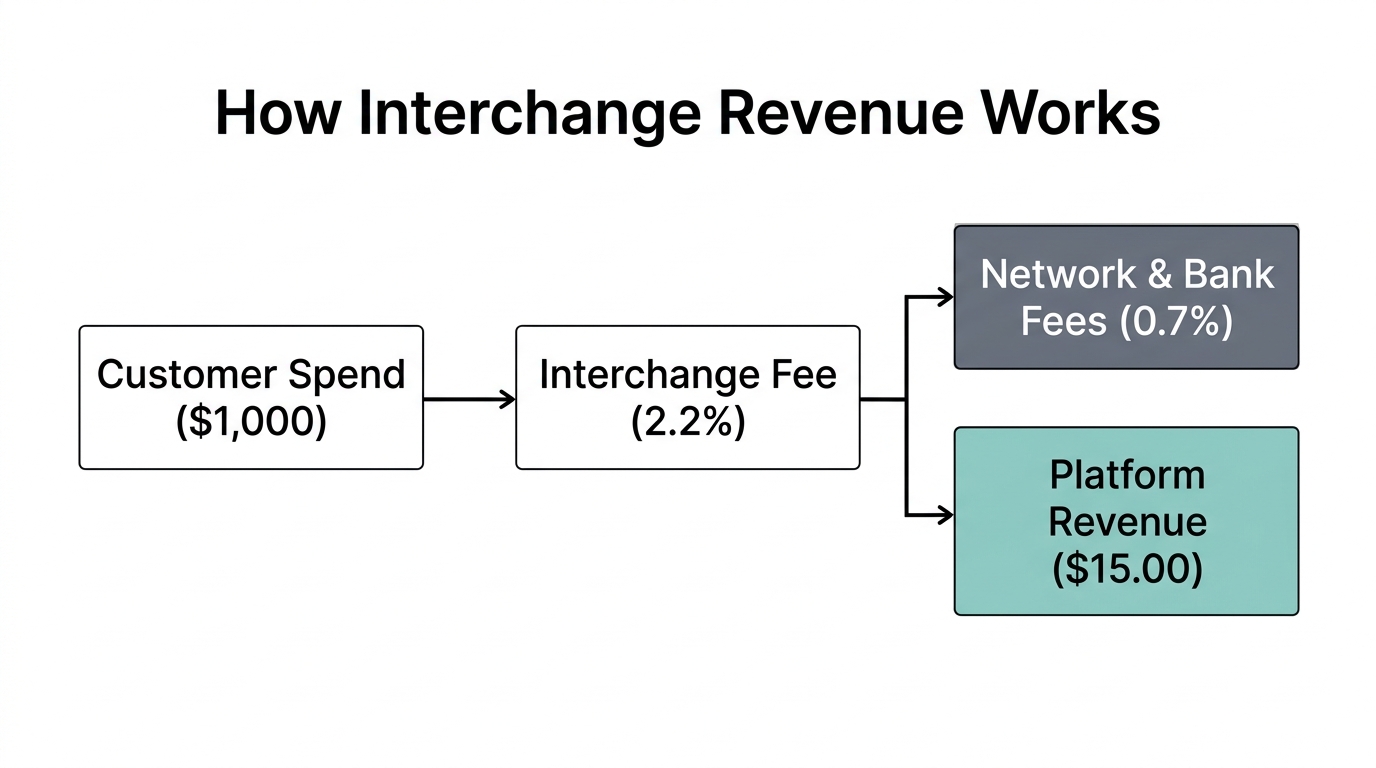

To understand how Ramp could offer a better product for free while growing at a 10% weekly rate, you have to understand the mechanics of interchange. Every time a card is swiped, a fee (usually around 2.9%) is split between various players. While companies like Stripe or Square take a small cut as the merchant processor, the issuer (the name on the card, like Ramp) keeps the lion's share of that fee.

| Role | Player Example | Estimated Net Take |

|---|---|---|

| Merchant Processor | Stripe / Square | 0.1% - 0.5% |

| Network | Visa / Mastercard | 0.1% - 0.4% |

| Issuer | Ramp / Chase | Majority of Interchange |

By capturing the issuer's portion of interchange, Ramp could fund the development of an elite software suite without charging a subscription fee. This financial engineering allowed them to reach a $100 million revenue run rate within just 15 to 17 months of hitting their first million. This velocity is unheard of in traditional banking. It allowed them to scale their team to over 1,100 people and manage billions in transaction volume while their competitors were still trying to figure out how to remove fax machines from their onboarding process.

Competitive Differentiation in 2026: Velocity as a Moat

Discover how Ramp disrupts legacy institutions through modern software innovation and superior speed.

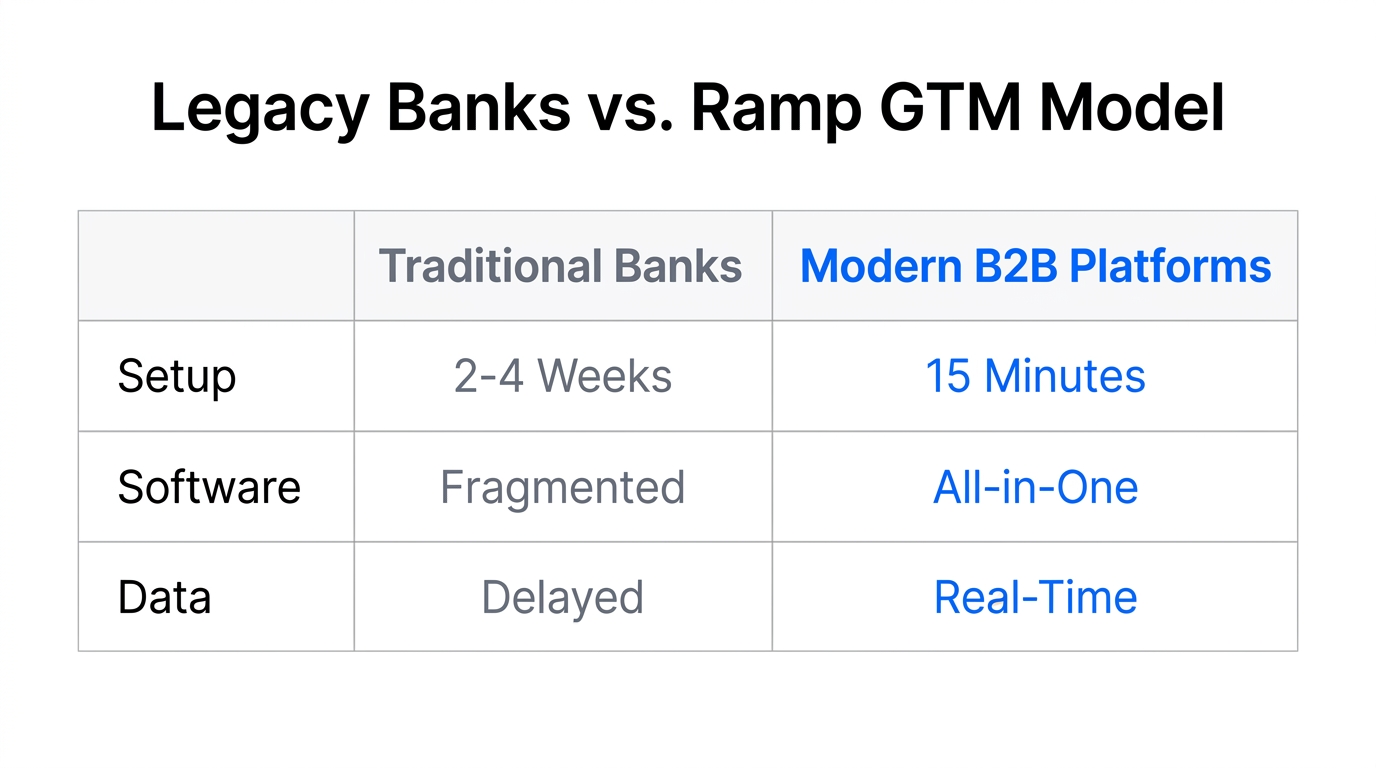

In 2026, brand power is a lagging indicator. While Amex relies on a 170-year-old brand, Ramp relies on shipping speed. Glyman notes that they count the days—literally. At one point, they were 2,310 days old, and every one of those days was spent optimizing a single function. This obsession with velocity is what allows a startup to outmaneuver an incumbent. While a legacy bank might take 18 months to approve a new feature, Ramp was approved by its network and funding its first transactions within 70 days of incorporation.

This speed isn't just about coding faster; it's about extreme focus. Much like how specialized platforms like Stormy AI have disrupted generalist marketing tools by focusing exclusively on AI-powered creator discovery and automated outreach, Ramp focused exclusively on the finance stack. They didn't try to be everything to everyone; they tried to be the fastest way to save money for a business. In 2026, if you aren't growing at least 20% a month in your early stages, you are likely being out-shipped by a competitor with a tighter feedback loop.

"The founders of our competitors wore top hats. They rely on the power of scale and time; we rely on the power of counting the days and shipping faster."

The Power of the 'All-in-One' Platform and LTV

One of the most effective customer retention strategies in B2B is consolidation. Fragmented tools lead to 'tool fatigue.' When Ramp combined cards, bill pay, reimbursements, and accounting into a single dashboard, they didn't just provide a service; they became the source of truth for the company's capital. This consolidation drives massive Lifetime Value (LTV) because the cost of switching away from an all-in-one system is incredibly high.

We see this trend across the 2026 tech stack. Companies are moving away from having 50 different micro-SaaS subscriptions. They want one platform for HR and Payroll (like Rippling), one for CRM (like HubSpot), and one for their creator economy operations (like Stormy AI). By abstracting away the 'paper cuts' of multiple logins and mismatched data, Ramp ensures that once a customer joins, they never have a reason to leave.

The 2026 GTM Playbook: Actionable Takeaways

Glyman breaks down his blank sheet approach to building and scaling a company.If you are looking to disrupt a legacy industry this year, the Ramp story provides a clear B2B go-to-market strategy framework:

- Identify the 'Paper Cuts': Don't look for a blue ocean; look for a red ocean where everyone is frustrated by manual tasks. Use VWO or similar tools to track where users drop off in existing legacy workflows.

- Build a Trojan Horse: Create a utility-first software tool that solves a problem immediately. Lead with value, not a sales pitch.

- Optimize for Velocity: Set aggressive goals (10% weekly growth) and design your team to ship daily. Use Zapier or Make to automate your internal operations so your humans can focus on the product.

- Consolidate the Stack: Look for fragmented tools in your niche and bring them under one roof. Whether it's finance or influencer marketing analytics, users want a single source of truth.

- Leverage Modern Financial Mechanics: Understand how money moves in your industry. Can you monetize via interchange, processing fees, or data instead of just a monthly SaaS fee?

Conclusion: The Future of B2B Disruption

Ramp's journey from a bold conversation between Eric and Karim to a $20 billion powerhouse is a testament to the power of software-led distribution. In 2026, the barrier to entry for legacy industries is no longer just capital; it's technological agility. By solving the boring problems that giants ignored, Ramp didn't just build a better credit card—they built a better way to run a business. Whether you're in fintech, healthcare, or creator marketing, the lesson is the same: find the friction, ship the solution, and count the days.